Blockchain serves as the foundation for cryptocurrencies and more. It's a decentralized ledger technology, recording transactions across many computers. Cryptocurrency is digital or virtual money, using cryptography for security. Bitcoin is a specific cryptocurrency, the first and most well-known one.

Blockchain, cryptocurrency, and Bitcoin often get used interchangeably, but they aren't the same. Each has unique features and roles in the digital world.

Understanding these differences is important. It helps you grasp the potential and limitations of each. As blockchain technology evolves, it impacts various industries beyond finance. Cryptocurrencies offer new ways to transact and invest. Bitcoin, as a pioneer, sets the stage for other digital currencies. Knowing how these elements connect and differ can guide your decisions in the digital economy.

Understanding the basics of blockchain is essential for anyone exploring cryptocurrency and Bitcoin. Blockchain technology forms the foundation of these digital currencies. Let's dive into what blockchain is and its key features.

Blockchain is a type of distributed ledger technology. It records transactions across many computers. This ensures the security and transparency of the data. Each record is called a "block". These blocks are linked together to form a "chain". Hence, the name blockchain.

Decentralization: No single entity controls the blockchain. It is managed by a network of computers.

Transparency: All transactions are visible to everyone on the network. This fosters trust and accountability.

Immutability: Once a transaction is recorded, it cannot be altered. This ensures the integrity of the data.

Security: Advanced cryptographic techniques protect the data. This makes it difficult for hackers to compromise the system.

Blockchain technology is the backbone of cryptocurrencies. Understanding its basics helps in grasping how digital currencies like Bitcoin operate.

Understanding the basics of cryptocurrency is essential in distinguishing between blockchain, cryptocurrency, and Bitcoin. The term cryptocurrency often comes up in discussions about digital finance and online transactions. Let's delve into its fundamentals to get a clearer picture.

A cryptocurrency is a digital or virtual currency. It uses cryptography for security. This makes it nearly impossible to counterfeit. Cryptocurrencies operate on decentralized networks based on blockchain technology. This means no central authority manages them.

Cryptocurrencies have unique features that set them apart. They are decentralized, meaning no single entity controls them. Transactions are verified through a process called mining. This ensures the integrity of the data. Cryptocurrencies offer anonymity. Users can make transactions without revealing their identity.

Another key characteristic is security. Advanced encryption techniques secure transactions. This reduces the risk of fraud. Cryptocurrencies also provide global access. Anyone with an internet connection can participate.

Understanding Bitcoin is crucial for grasping the broader concepts of blockchain and cryptocurrency. Bitcoin, often confused with blockchain and cryptocurrency, has its unique features and origins. Let's delve into the essentials of Bitcoin, focusing on its origin and key attributes.

Bitcoin was introduced in 2008 by an unknown person or group using the name Satoshi Nakamoto. It was created as a response to the financial crisis. The first Bitcoin block, known as the Genesis Block, was mined in January 2009. This marked the birth of the first decentralized digital currency.

Bitcoin aimed to provide a peer-to-peer electronic cash system. This system allowed online payments to be sent directly from one party to another. No financial institution was needed. It solved the problem of double-spending using cryptographic proof.

Bitcoin has several key attributes that make it unique:

Decentralization: No central authority controls Bitcoin. Transactions are verified by network nodes through cryptography.

Limited Supply: The total supply of Bitcoin is capped at 21 million. This scarcity is designed to increase its value over time.

Security: Bitcoin transactions are secure and irreversible. It uses blockchain technology to ensure transparency and security.

Transparency: All Bitcoin transactions are recorded on a public ledger. This ledger is accessible to anyone.

Divisibility: One Bitcoin can be divided into 100 million smaller units, called satoshis. This makes it possible to conduct small transactions.

These attributes have contributed to Bitcoin's popularity and adoption worldwide. It has become a store of value, often referred to as "digital gold".

Credit: shardeum.org

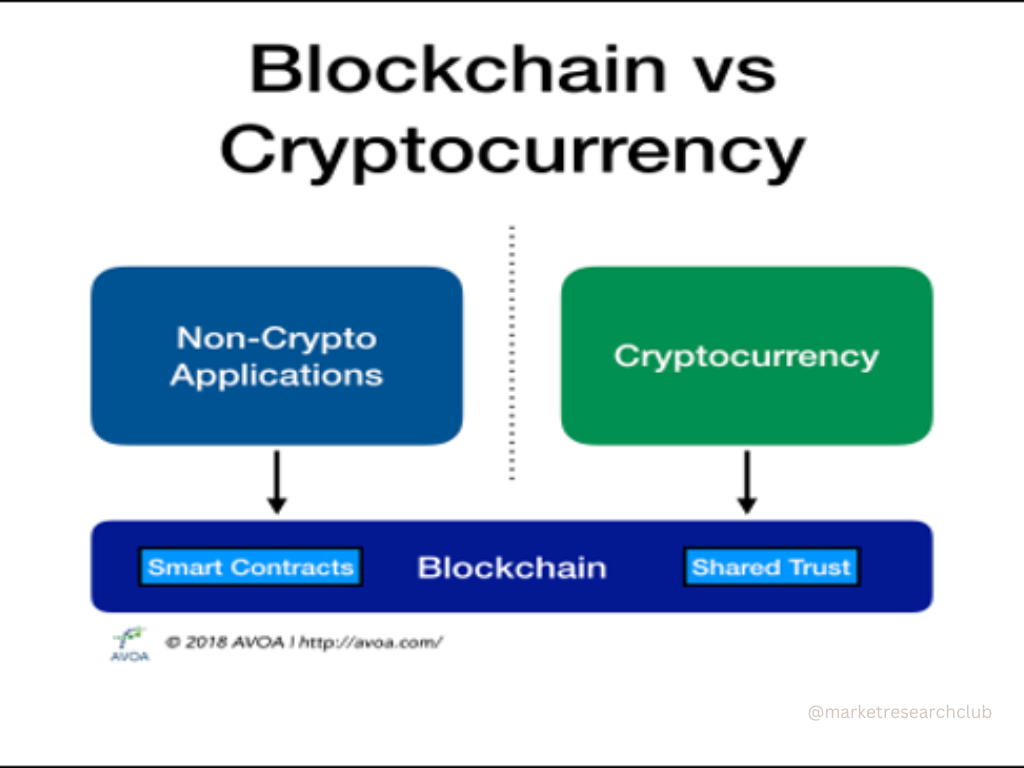

Blockchain and cryptocurrency are terms often used interchangeably. They are not the same. Understanding their differences is crucial for anyone interested in digital finance. Let's dive into the core differences and use cases of blockchain and cryptocurrency.

Blockchain is a technology. It records transactions across many computers. This system ensures transparency and security. Cryptocurrency is a digital asset. It uses blockchain to secure and verify transactions. Bitcoin is a type of cryptocurrency.

Blockchain provides the foundation for cryptocurrencies. It acts as a public ledger. Cryptocurrencies rely on this ledger to function. Without blockchain, cryptocurrencies like Bitcoin wouldn't exist. Blockchain can be used for other purposes too.

Blockchain has many uses beyond cryptocurrency. Businesses use blockchain for supply chain tracking. It helps in verifying product authenticity. Voting systems use blockchain to ensure fair elections. Healthcare uses it for secure patient records.

Cryptocurrency's primary use is digital transactions. People buy, sell, and trade goods using cryptocurrencies. Bitcoin is the most popular for this purpose. Some use cryptocurrencies for investment. They hope the value will increase over time.

While blockchain and cryptocurrency are connected, they serve different purposes. Blockchain is the technology. Cryptocurrency is one of its applications. Understanding this helps in grasping their potential and limitations.

Blockchain and Bitcoin are often mentioned together. Many people think they are the same. But they are not. Blockchain is a technology. Bitcoin is a digital currency. Let's explore their differences.

Blockchain is a system for recording data. It is decentralized and secure. It uses blocks to store information. Each block links to the previous one. This forms a chain.

Bitcoin is a type of cryptocurrency. It uses blockchain technology. Bitcoin is a digital form of money. It is not controlled by any government or bank.

Blockchain is versatile. It can support various applications. These include supply chain management, voting systems, and more. It enhances transparency and security.

Bitcoin focuses on financial transactions. It allows peer-to-peer payments. Users can send money without middlemen. This reduces transaction fees.

Blockchain provides the foundation. Bitcoin is one of its applications. Blockchain's potential is vast. Bitcoin's use case is specific.

Credit: www.digitalx.com

Understanding the difference between Cryptocurrency and Bitcoin is essential for anyone new to the world of digital currency. Though the two terms are often used interchangeably, they are not the same. Bitcoin is a type of cryptocurrency, but not all cryptocurrencies are Bitcoin.

Cryptocurrency is a broad term that refers to digital or virtual currencies that use cryptography for security. They operate on decentralized networks using blockchain technology. Bitcoin, on the other hand, is the first and most well-known cryptocurrency. It was created by an unknown person or group using the name Satoshi Nakamoto in 2009.

Here are the main differences:

|

Feature |

Cryptocurrency |

Bitcoin |

|---|---|---|

|

Definition |

Digital or virtual currencies using cryptography |

The first and most well-known cryptocurrency |

|

Creator |

Various developers and teams |

Satoshi Nakamoto |

|

Examples |

Ethereum, Litecoin, Ripple |

Bitcoin |

While Bitcoin is the most famous, many other cryptocurrencies exist. These offer different features and advantages.

Ethereum: Known for its smart contract functionality.

Litecoin: Offers faster transaction times compared to Bitcoin.

Ripple: Focuses on enabling real-time, cross-border payments.

Each of these cryptocurrencies serves unique purposes and operates on different protocols. They contribute to the diverse landscape of digital currencies.

Understanding blockchain, cryptocurrency, and Bitcoin can be tricky. Many believe these terms mean the same thing. This confusion leads to common misconceptions. Let's clear up these misunderstandings and clarify the differences.

Some think blockchain and Bitcoin are the same. They also believe all cryptocurrencies are Bitcoin. These are common misconceptions. Blockchain is the technology behind cryptocurrencies. Bitcoin is just one type of cryptocurrency.

Others assume that using Bitcoin means using blockchain. This is not always true. Blockchain has many uses beyond Bitcoin. It can track supply chains or manage contracts. This misunderstanding limits the view of blockchain's potential.

Blockchain is a digital ledger. It records transactions in a secure way. Each entry, or block, links to the previous one. This creates a chain. Hence the name, blockchain. It is not limited to financial data. It can store any type of data.

Cryptocurrency is digital money. It uses cryptography for security. Bitcoin is the first and most well-known cryptocurrency. But many other cryptocurrencies exist. Ethereum and Litecoin are examples. They use blockchain technology too.

So, blockchain is the technology. Cryptocurrency is the application. Bitcoin is just one example of a cryptocurrency. Understanding these differences helps avoid confusion. It also shows the broad potential of blockchain technology.

Credit: www.digitalx.com

The future outlook for blockchain, cryptocurrency, and Bitcoin is a topic of great interest. As technology advances, these digital assets continue to evolve. Understanding their future helps in making informed decisions and staying ahead in the digital age.

Experts predict blockchain technology will expand beyond finance. It may transform various industries like healthcare, supply chain, and real estate. Blockchain's transparent and secure nature makes it appealing for record-keeping and data management.

Cryptocurrencies are expected to gain wider acceptance. More businesses might start accepting them as payment. This could include both online and physical stores. The move could drive mainstream adoption and increase their value.

Bitcoin, being the most well-known cryptocurrency, could see significant growth. Some believe it might become a global digital currency. Others think it will remain a store of value like gold. Its future largely depends on market trends and regulatory changes.

Blockchain technology faces several challenges. One major issue is scalability. Current blockchain networks struggle with processing large volumes of transactions. This can lead to slower speeds and higher costs.

Another challenge is regulation. Governments around the world are still figuring out how to regulate cryptocurrencies. Unclear or strict regulations could hinder growth and adoption.

Security remains a concern for both blockchain and cryptocurrencies. While blockchain is generally secure, it's not immune to attacks. Hackers constantly find new ways to exploit vulnerabilities. Ensuring robust security measures is crucial for trust and adoption.

Bitcoin also faces specific challenges. Its high volatility makes it a risky investment. Price fluctuations can deter people from using it as a stable currency. Additionally, Bitcoin's energy consumption is a growing concern. Its mining process requires a lot of electricity, raising environmental issues.

No, Bitcoin and blockchain are not the same. Bitcoin is a cryptocurrency, while blockchain is the technology behind it. Blockchain records transactions securely. Bitcoin uses blockchain for its operations.

No, bitcoins and cryptocurrency are not the same. Bitcoin is a type of cryptocurrency, while cryptocurrency refers to all digital currencies.

Blockchain offers transparency, security, and decentralization. It reduces fraud and enhances traceability. High energy use and scalability issues are cons.

No, a blockchain is not a cryptocurrency. Blockchain is the technology behind cryptocurrencies. Cryptocurrencies are digital assets using blockchain for transactions.

Understanding blockchain, cryptocurrency, and Bitcoin is important. Blockchain is the technology. Cryptocurrencies are digital currencies. Bitcoin is the first cryptocurrency. These concepts might seem complex, but they are interconnected. Blockchain secures and records transactions. Cryptocurrencies operate on blockchain. Bitcoin remains the most popular example.

Knowing these differences helps in grasping the digital finance world. Stay informed, and keep learning about these innovations. They shape the future of finance.

Napa Extra is a term that piques curiosity. What exactly is Napa Extra? Napa Valley is renowned for its exquisite wines, picturesque landscapes, and vibrant culture. Napa Extra delves deeper into the unique aspects that make Napa Valley stand out. This guide will explore the hidden gems, extraordinary experiences, and must-visit spots in this iconic region. Whether you're a wine lover, a foodie, or an adventure seeker, there's something special here for everyone. Let's uncover the best of Napa Extra and see what makes it such a remarkable destination.

The internet is vast and often misunderstood. Within it, there are three main layers: the Clear Web, Deep Web, and Dark Web. Each serves different purposes and has unique characteristics. The Clear Web is the surface internet we use daily. It includes websites indexed by search engines like Google. The Deep Web, although not indexed, holds private data and academic resources. It's much larger than the Clear Web. The Dark Web, a hidden part of the Deep Web, is accessed through special browsers. It’s known for anonymous activities, both legal and illegal. Understanding these layers helps you navigate the internet safely and responsibly. This blog post will explore these layers in detail, shedding light on their key differences and uses.

Making money with the Binance trading bot is possible. It involves using automated strategies. This guide will help you understand how. Trading bots are tools that execute trades for you. They use algorithms to buy and sell based on market trends. For beginners, it can be a great way to start trading without deep market knowledge. With Binance, one of the world's largest crypto exchanges, you have access to powerful trading bots. These bots can work 24/7, making trades while you sleep. In this post, you will learn the basics of using these bots. We will cover setup, strategies, and tips to maximize profits. Ready to dive in? Let's explore how you can make money with the Binance trading bot.

How many Pi Network coins are there in the world? Currently, there is no fixed total, as the number of coins continues to grow. The Pi Network is unique, allowing users to mine coins through their mobile devices, which adds to its dynamic nature. The Pi Network has attracted significant attention in the cryptocurrency space. Launched in 2019, it aims to make digital currency accessible to everyone. Unlike traditional cryptocurrencies, which require expensive hardware, Pi coins can be mined simply by using an app on your phone. This innovative approach has led to millions of users participating in the network. However, the total number of coins in existence remains a topic of curiosity and debate. Understanding this can provide insights into the potential value and future of Pi coins in the global market.

Cricket fans, brace yourselves! The ICC Champions Trophy 2025 is around the corner. One of the most anticipated matches is Bangladesh vs New Zealand. This clash promises excitement, skill, and unforgettable moments. The ICC Champions Trophy always brings thrilling cricket action. Bangladesh and New Zealand have shown impressive performances in past tournaments. This match-up is expected to be fierce, with both teams eager to prove their mettle. Bangladesh, with its rising cricket stars, aims to make a mark on the international stage. New Zealand, known for their consistent and strategic play, looks to maintain their dominance. Fans worldwide are eager to see these teams compete. Who will emerge victorious? The stakes are high, and the excitement is palpable.

Cricket fans are eagerly waiting for the ICC Champions Trophy 2025. The biggest highlight? The epic clash between India and Pakistan. The rivalry between India and Pakistan in cricket is legendary. This match promises intense excitement and high drama. Millions of fans will be glued to their screens, cheering passionately. The history between these two teams adds extra spice. Their battles on the cricket field are always fierce and memorable. As the ICC Champions Trophy 2025 approaches, anticipation builds. Each team aims to outshine the other and claim victory. Get ready for an unforgettable showdown. This clash is not just a game; it's a spectacle that captures the hearts of millions. Stay tuned for a thrilling ride!

The Nobel Prize is one of the most prestigious awards in the world. It honors outstanding contributions in various fields. The anticipation surrounding the Nobel Prize nominees and winners for 2025 is already building. Every year, exceptional individuals and organizations are recognized for their remarkable achievements. From groundbreaking scientific discoveries to profound literary works, the Nobel Prize celebrates those who have significantly impacted society. This year promises to be no different, with many deserving candidates in the running. As we await the announcement, let's explore the significance of this esteemed award and the incredible individuals who may be honored. The Nobel Prize acknowledges excellence and inspires future generations to strive for greatness.

Creating an NFT art app in 2025 is a promising venture. As NFTs grow in popularity, many seek ways to enter this digital space. NFTs, or non-fungible tokens, are unique digital items stored on a blockchain. They have revolutionized the art world, offering artists new ways to sell and protect their work. In 2025, building an NFT art app can be a great opportunity for developers and artists alike. This guide will walk you through the essential steps to create a successful app. We'll cover the basics, from understanding the technology to the tools you'll need. By the end, you'll have a clear roadmap to bring your NFT art app to life. Let's dive in!

Machine learning and artificial intelligence (AI) are changing many fields. One key area is the procurement supply chain. In the world of procurement, efficiency and accuracy are crucial. Machine learning and AI help achieve both. These technologies can predict demand, manage inventory, and optimize operations. They reduce human errors and save time. Understanding their role in procurement is essential. In this blog, we'll explore how machine learning and AI transform the supply chain. This knowledge will help you see the potential benefits and prepare for the future. Stay tuned to learn more about this exciting topic.

Creating subtitles for videos using AI is simple and efficient. AI tools can save you time and improve accuracy. Videos with subtitles reach a broader audience. They help those who are deaf or hard of hearing. Subtitles also aid in understanding for non-native speakers. AI technology has made it easier than ever to add subtitles to your videos. With just a few clicks, you can generate accurate subtitles. You no longer need to type out every word manually. This post will guide you through the process. You will learn how to use AI tools to create subtitles. The steps are easy to follow. Let's dive in and see how you can enhance your videos with AI-generated subtitles.